CBRE trades at $127.50 per share and has moved almost in lockstep with the market over the last six months. The stock has lost 5.9% while the S&P 500 is down 2.1%. This may have investors wondering how to approach the situation.

Is there a buying opportunity in CBRE, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think CBRE Will Underperform?

Even with the cheaper entry price, we're swiping left on CBRE for now. Here are three reasons why we avoid CBRE and a stock we'd rather own.

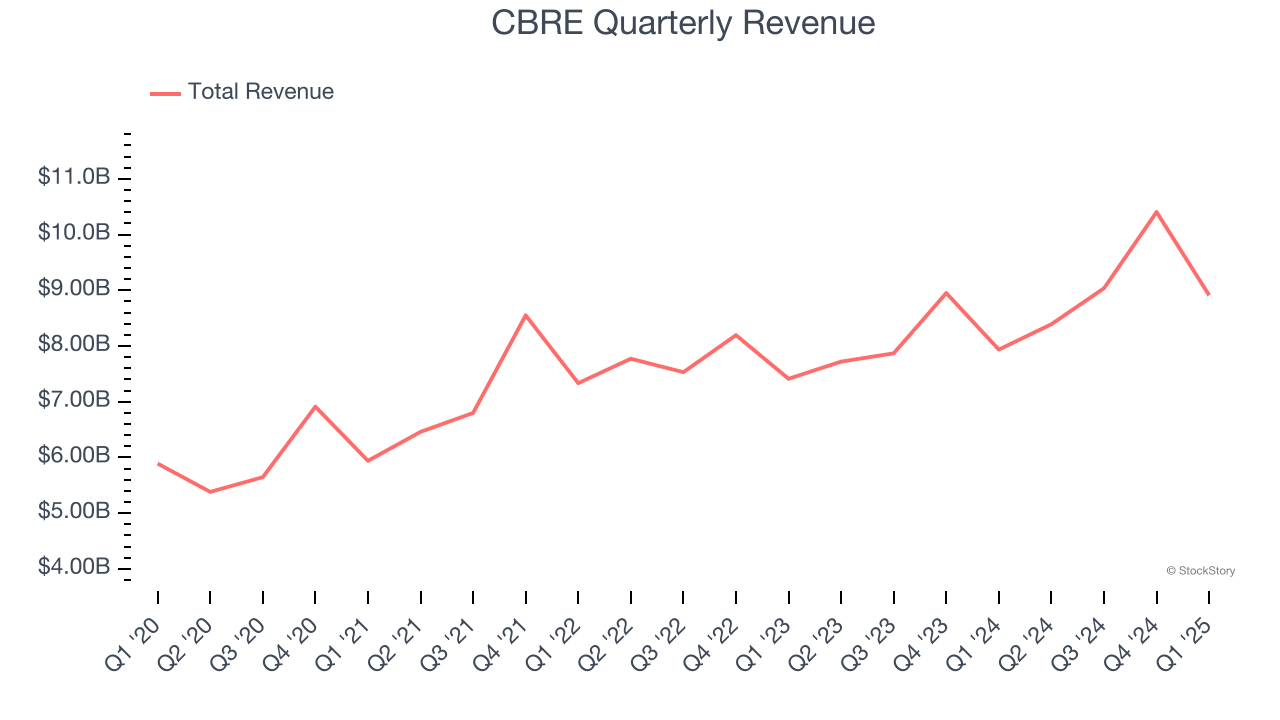

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, CBRE grew its sales at a sluggish 8.3% compounded annual growth rate. This fell short of our benchmark for the consumer discretionary sector.

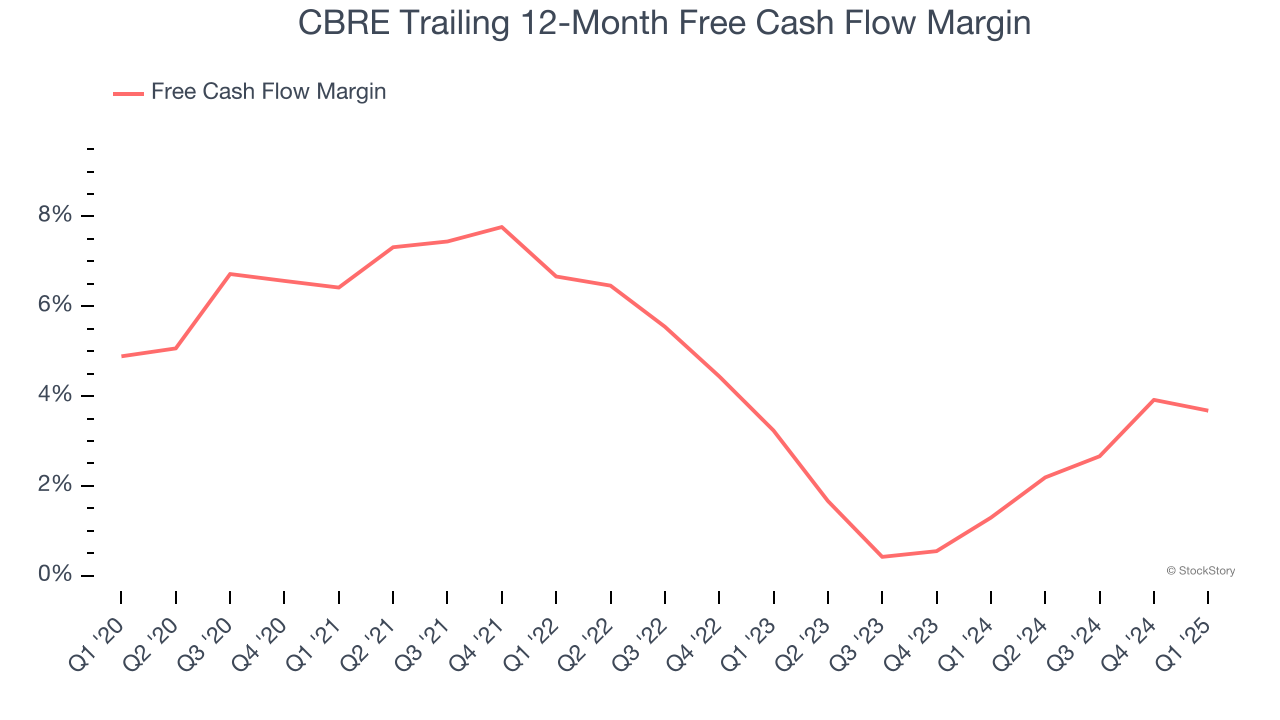

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

CBRE has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.6%, lousy for a consumer discretionary business.

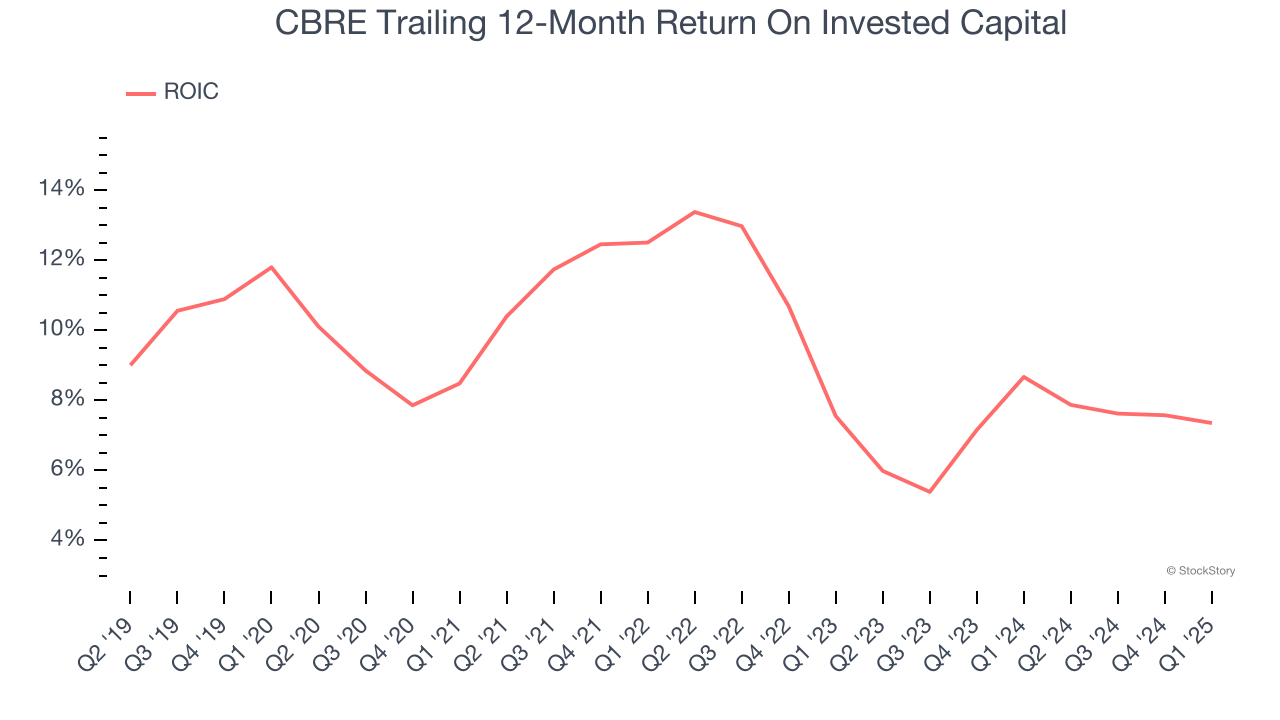

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

CBRE historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 8.9%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of CBRE, we’ll be cheering from the sidelines. Following the recent decline, the stock trades at 19.7× forward P/E (or $127.50 per share). At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.