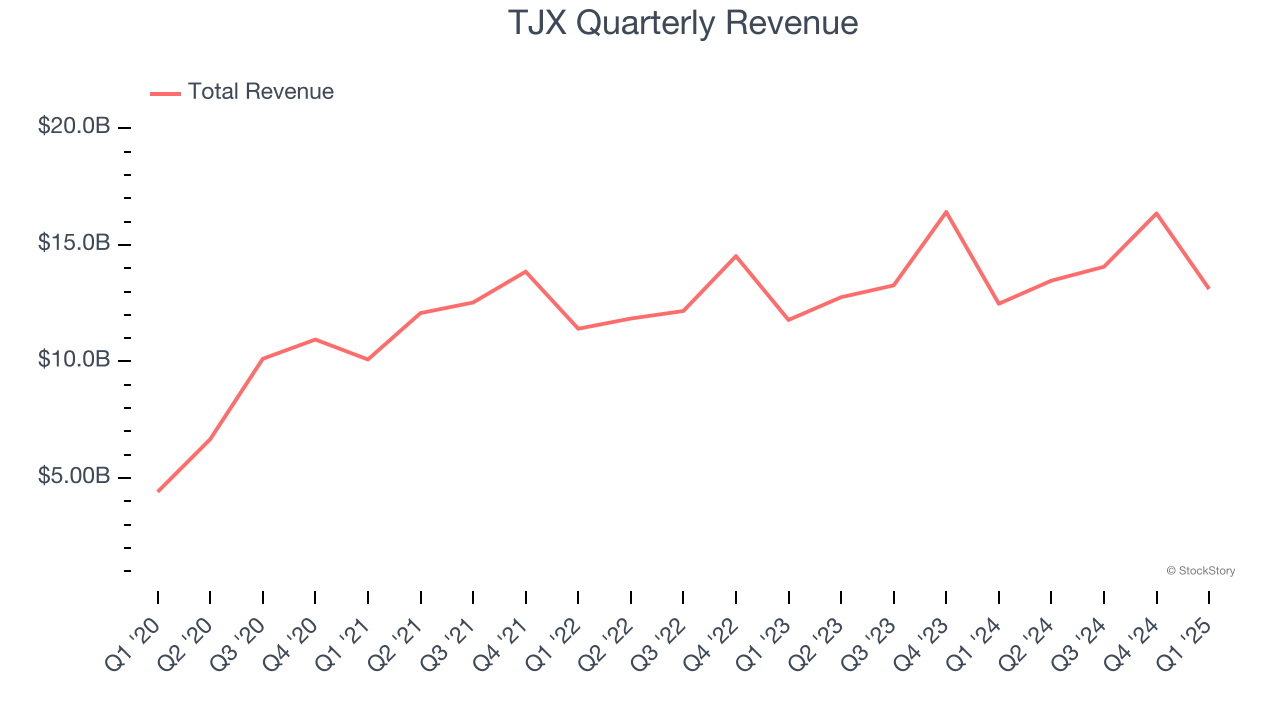

Off-price retail company TJX (NYSE:TJX) reported Q1 CY2025 results exceeding the market’s revenue expectations, with sales up 5.1% year on year to $13.11 billion. On the other hand, next quarter’s revenue guidance of $13.8 billion was less impressive, coming in 2% below analysts’ estimates. Its GAAP profit of $0.92 per share was in line with analysts’ consensus estimates.

Is now the time to buy TJX? Find out by accessing our full research report, it’s free.

TJX (TJX) Q1 CY2025 Highlights:

- Revenue: $13.11 billion vs analyst estimates of $13.02 billion (5.1% year-on-year growth, 0.7% beat)

- EPS (GAAP): $0.92 vs analyst estimates of $0.91 (in line)

- Adjusted EBITDA: $1.38 billion vs analyst estimates of $1.57 billion (10.5% margin, 12.4% miss)

- Revenue Guidance for Q2 CY2025 is $13.8 billion at the midpoint, below analyst estimates of $14.08 billion

- EPS (GAAP) guidance for the full year is $4.39 at the midpoint, missing analyst estimates by 2.7%

- Operating Margin: 10%, in line with the same quarter last year

- Free Cash Flow was -$103 million, down from $318 million in the same quarter last year

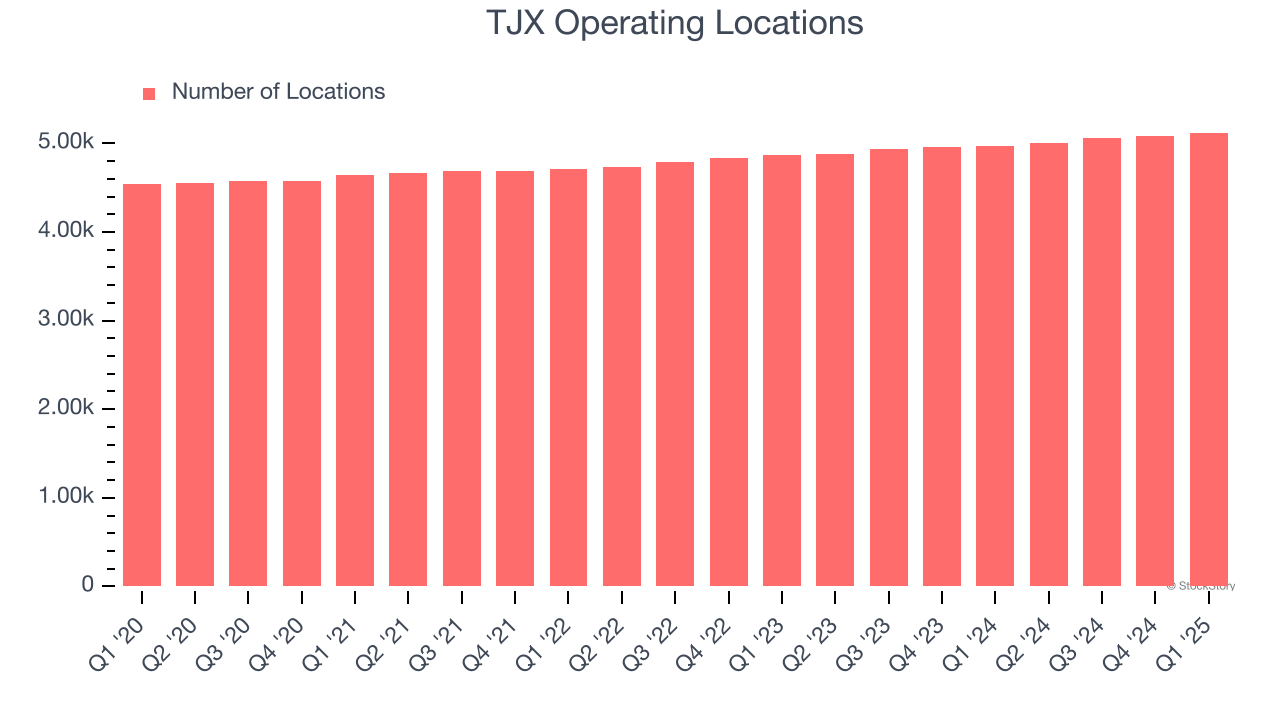

- Locations: 5,121 at quarter end, up from 4,972 in the same quarter last year

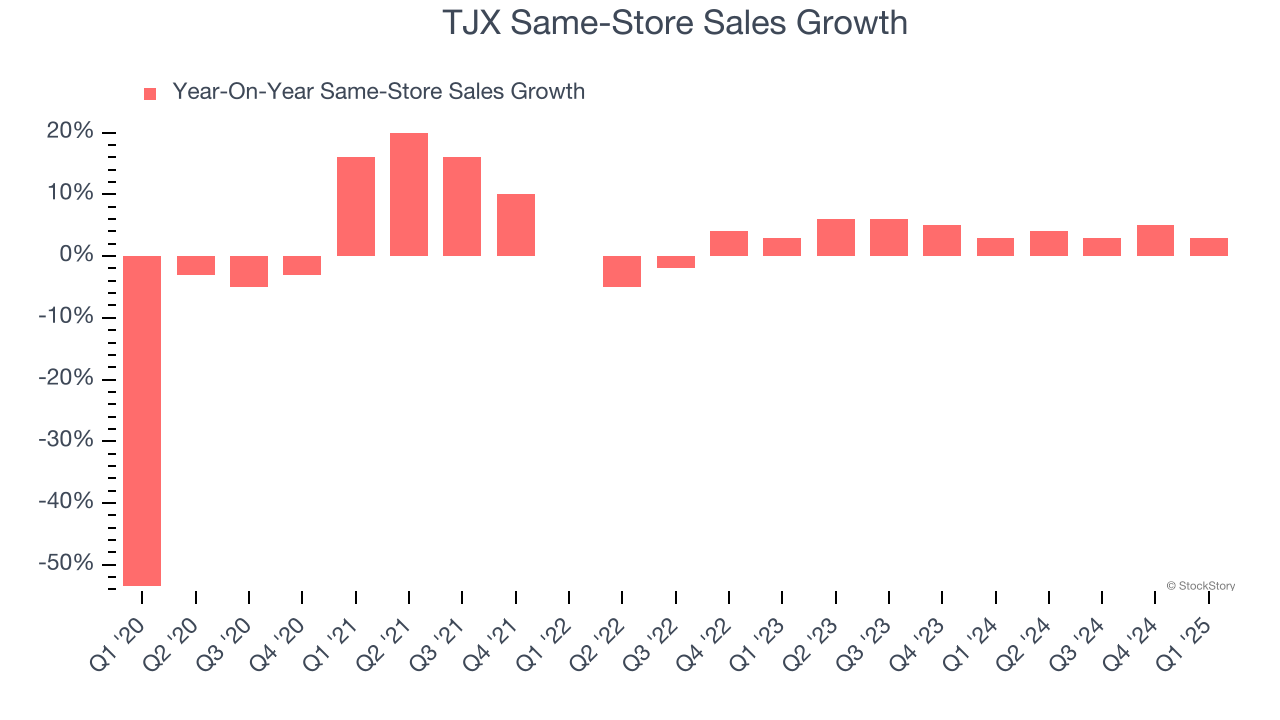

- Same-Store Sales rose 3% year on year, in line with the same quarter last year

- Market Capitalization: $150.6 billion

Ernie Herrman, Chief Executive Officer and President of The TJX Companies, Inc., stated, “I am very pleased with our first quarter performance. Overall comp sales increased 3%, at the high end of our plan, and both profitability and earnings per share were above our expectations. Our teams across the Company delivered consumers exciting values on great brands and fashions and a treasure-hunt shopping experience, every day. All divisions, both in the U.S. and internationally, drove increases in comp sales and customer transactions, which underscores the strength of our value proposition. This also gives us confidence in our ability to gain market share across all of our geographies. The second quarter is off to a strong start and we are laser focused on executing all the key fundamentals of our off-price retail model. I am convinced that our broad assortments of great brands and fashions, at compelling prices, will continue to be a tremendous draw for shoppers seeking value. Further, I am confident that the strength, flexibility, and resiliency of our off-price business model will serve us well in today’s macro environment, as it has throughout our long, successful history. I am as confident as ever that we will bring our value proposition to even more customers around the world and keep growing our sales and profitability over the long term.”

Company Overview

Initially based on a strategy of buying excess inventory from manufacturers or other retailers, TJX (NYSE:TJX) is an off-price retailer that sells brand-name apparel and other goods at prices much lower than department stores.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $56.99 billion in revenue over the past 12 months, TJX is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because there are only a finite number of places to build new stores, making it harder to find incremental growth. To accelerate sales, TJX likely needs to optimize its pricing or lean into international expansion.

As you can see below, TJX’s 6.3% annualized revenue growth over the last six years (we compare to 2019 to normalize for COVID-19 impacts) was tepid, but to its credit, it opened new stores and increased sales at existing, established locations.

This quarter, TJX reported year-on-year revenue growth of 5.1%, and its $13.11 billion of revenue exceeded Wall Street’s estimates by 0.7%. Company management is currently guiding for a 2.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months, a slight deceleration versus the last six years. We still think its growth trajectory is attractive given its scale and suggests the market is forecasting success for its products.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

TJX operated 5,121 locations in the latest quarter. It has opened new stores quickly over the last two years, averaging 2.7% annual growth, faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

TJX’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 4.4% per year. This performance suggests its rollout of new stores is beneficial for shareholders. We like this backdrop because it gives TJX multiple ways to win: revenue growth can come from new stores, e-commerce, or increased foot traffic and higher sales per customer at existing locations.

In the latest quarter, TJX’s same-store sales rose 3% year on year. This growth was a deceleration from its historical levels, showing the business is still performing well but losing a bit of steam.

Key Takeaways from TJX’s Q1 Results

It was good to see TJX narrowly top analysts’ revenue expectations this quarter. On the other hand, its EBITDA missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.2% to $132.05 immediately after reporting.

TJX underperformed this quarter, but does that create an opportunity to invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.