As the Q3 earnings season wraps, let’s dig into this quarter’s best and worst performers in the dental equipment & technology industry, including Align Technology (NASDAQ:ALGN) and its peers.

The dental equipment and technology industry encompasses companies that manufacture orthodontic products, dental implants, imaging systems, and digital tools for dental professionals. These companies benefit from recurring revenue streams tied to consumables, ongoing maintenance, and growing demand for aesthetic and restorative dentistry. However, high R&D costs, significant capital investment requirements, and reliance on discretionary spending make them vulnerable to economic cycles. Over the next few years, tailwinds for the sector include innovation in digital workflows, such as 3D printing and AI-driven diagnostics, which enhance the efficiency and precision of dental care. However, headwinds include economic uncertainty, which could reduce patient spending on elective procedures, regulatory challenges, and potential pricing pressures from consolidated dental service organizations (DSOs).

The 4 dental equipment & technology stocks we track reported a strong Q3. As a group, revenues beat analysts’ consensus estimates by 2.3% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 1.4% on average since the latest earnings results.

Align Technology (NASDAQ:ALGN)

Pioneering an alternative to traditional metal braces with nearly invisible plastic aligners, Align Technology (NASDAQ:ALGN) designs and manufactures Invisalign clear aligners, iTero intraoral scanners, and dental CAD/CAM software for orthodontic and restorative treatments.

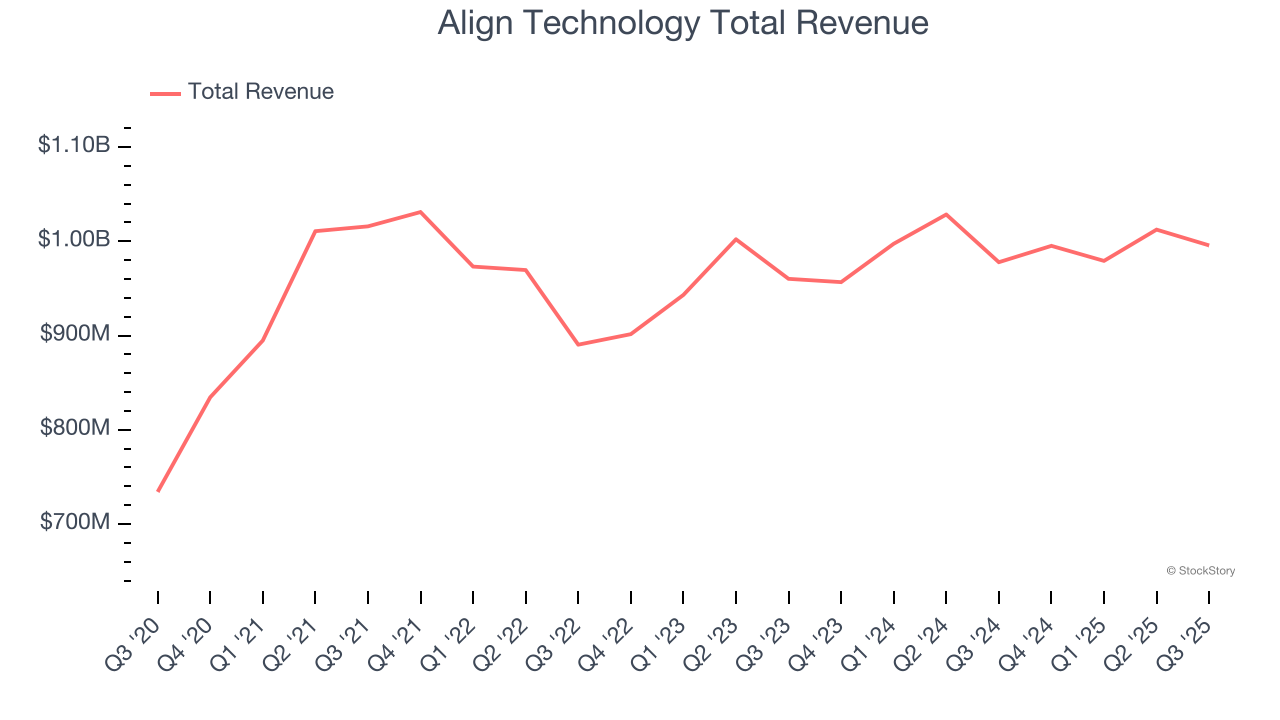

Align Technology reported revenues of $995.7 million, up 1.8% year on year. This print exceeded analysts’ expectations by 2.2%. Overall, it was a strong quarter for the company with an impressive beat of analysts’ revenue estimates and a beat of analysts’ EPS estimates.

Interestingly, the stock is up 8.1% since reporting and currently trades at $142.56.

Is now the time to buy Align Technology? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q3: Envista (NYSE:NVST)

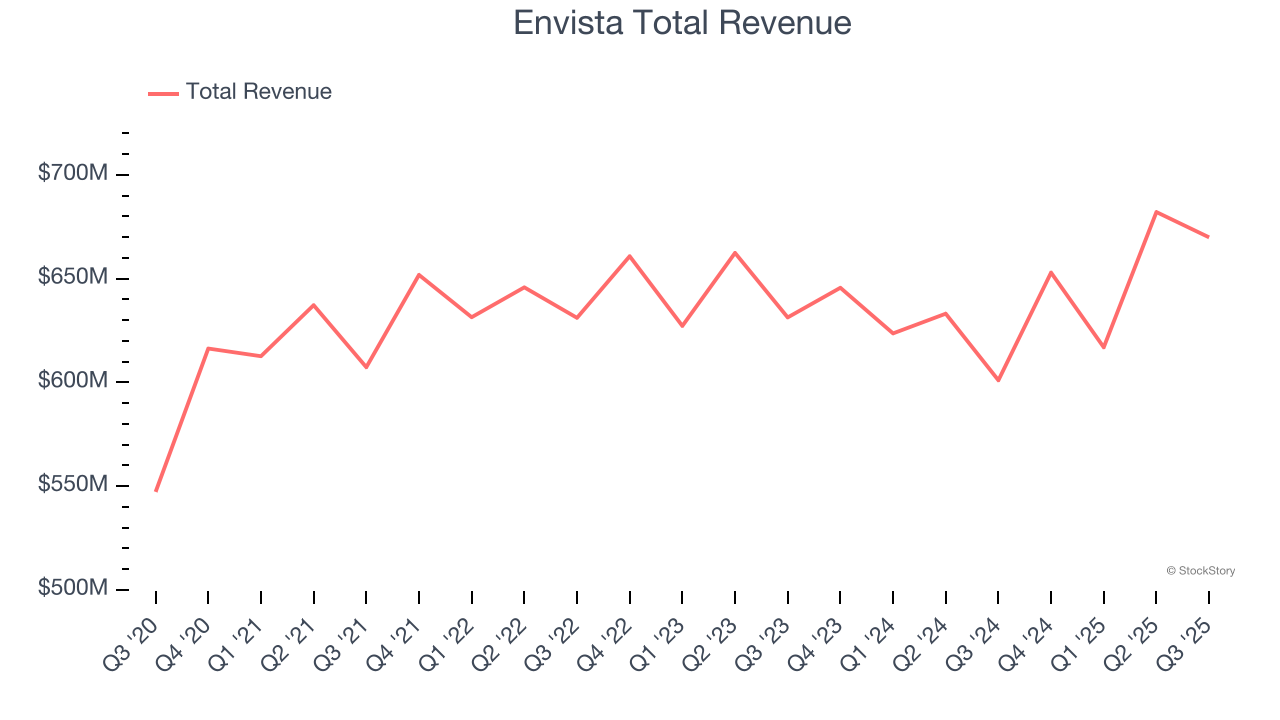

Uniting more than 30 trusted brands including Nobel Biocare, Ormco, and DEXIS under one corporate umbrella, Envista Holdings (NYSE:NVST) is a global dental products company that provides equipment, consumables, and specialized technologies for dental professionals.

Envista reported revenues of $669.9 million, up 11.5% year on year, outperforming analysts’ expectations by 4.6%. The business had an exceptional quarter with a solid beat of analysts’ constant currency revenue estimates and an impressive beat of analysts’ revenue estimates.

Envista scored the biggest analyst estimates beat and fastest revenue growth among its peers. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $19.89.

Is now the time to buy Envista? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Dentsply Sirona (NASDAQ:XRAY)

With roots dating back to 1877 when it introduced the first dental electric drill, Dentsply Sirona (NASDAQ:XRAY) manufactures and sells professional dental equipment, technologies, and consumable products used by dentists and specialists worldwide.

Dentsply Sirona reported revenues of $904 million, down 4.9% year on year, exceeding analysts’ expectations by 0.5%. Still, it was a softer quarter as it posted a significant miss of analysts’ full-year EPS guidance estimates and a significant miss of analysts’ EPS estimates.

Dentsply Sirona delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 15.5% since the results and currently trades at $10.67.

Read our full analysis of Dentsply Sirona’s results here.

Henry Schein (NASDAQ:HSIC)

With a vast inventory of over 300,000 products stocked in distribution centers spanning more than 5.3 million square feet worldwide, Henry Schein (NASDAQ:HSIC) is a global distributor of healthcare products and services primarily to dental practices, medical offices, and other healthcare facilities.

Henry Schein reported revenues of $3.34 billion, up 5.2% year on year. This print beat analysts’ expectations by 1.9%. It was a strong quarter as it also put up a solid beat of analysts’ full-year EPS guidance estimates and a decent beat of analysts’ revenue estimates.

The stock is up 13.5% since reporting and currently trades at $73.40.

Read our full, actionable report on Henry Schein here, it’s free for active Edge members.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.